The Weight Threshold: Every commercial motor vehicle (CMV) tracking a taxable gross weight of 55,000 pounds or more is legally required to submit an annual IRS Form 2290.

Filing Windows: The standard tax cycle spans from July 1st to June 30th of the following calendar year, with your annual return due explicitly by August 31st.

The Registration Gatekeeper: State DMVs and International Registration Plan (IRP) agencies will refuse to issue or renew commercial license plates without a validated, IRS-stamped Schedule 1.

Exclusively EIN: The IRS strictly rejects Form 2290 filings submitted under personal Social Security Numbers (SSNs); you must utilize a dedicated Employer Identification Number.

Prorated Billing: Vehicles deployed on public roads mid-cycle are subject to a customized prorated tax calculation determined solely by the vehicle’s specific Month of First Use.

Juggling hours-of-service (HOS) tracking, fluctuating diesel overhead, and freight dispatch coordinates can leave independent owner-operators with little bandwidth for administrative red tape. Yet, ignoring federal excise obligations can instantly derail an active trucking operation. If you operate an over-the-road asset with a taxable gross weight scaling 55,000 pounds or higher, completing your Heavy Vehicle Use Tax (HVUT) return is an unavoidable milestone. Failing to submit your annual tax paperwork doesn’t just invite standard IRS interest assessments; it triggers a systemic block at state Department of Motor Vehicles (DMV) desks and International Registration Plan (IRP) offices, completely revoking your ability to secure or renew your commercial license plates.

According to administrative compliance studies, up to 15% of first-time owner-operators experience unnecessary freight delays during mid-summer peak registration renewals. These delays typically stem from a single error: relying on outdated, paper-mailed tax filings that leave operations stranded in a six-week federal processing backlog. For an independent driver whose cash flow depends entirely on active wheel rotation, that kind of administrative standstill can be financially devastating. This complete guide to

Form 2290 e-filing for owner operators: complete HVUT guide provides the technical strategies, calculation models, and filing steps you need to secure your stamped Schedule 1 in minutes, satisfying both the IRS and state compliance inspectors

Deconstructing the Taxable Gross Weight Equation

A common trap for independent owner-operators is mistaking empty tractor weight or standard scale-ticket weights for the vehicle’s formal IRS taxable gross weight. The IRS evaluates your equipment using a specific structural combination framework.

The Three-Tier Weight Formula

To determine your vehicle’s correct weight category, you must add together three separate values:

- The base unladen weight of the fully equipped truck-tractor ready for service.

- The unladen weight of the standard trailer or semi-trailer configuration typically hitched to the unit.

- The maximum payload weight customarily hauled by the combination across public highways.

If your calculated combination total lands at 54,999 pounds or less, you are entirely exempt from the heavy vehicle use tax framework. However, the moment your combination crosses the 55,000-pound threshold, your vehicle shifts into Category A, and your tax liability scales upward in 5,000-pound steps until peaking at 75,000+ pounds (Category V).

Evaluating the Form 2290 Prorated Tax Table

The standard annual tax assessment for a max-gross commercial motor vehicle (Category V, over 75,000 lbs) is capped at $550. Commercial logging trucks receive a designated statutory discount, capping out at a maximum of $412.50.

However, if you purchase a new asset or change your operating authority mid-cycle, your financial obligation is prorated based on your specific Month of First Use (FUM).

| Month of First Use | Electronic Filing Deadline | Remaining Active Months | Prorated Tax Due |

|---|---|---|---|

| July | August 31st | 12 Months | $550.00 |

| August | September 30th | 11 Months | $504.17 |

| September | October 31st | 10 Months | $458.33 |

| October | November 30th | 9 Months | $412.50 |

| November | December 31st | 8 Months | $366.67 |

| December | January 31st | 7 Months | $320.83 |

| January | February 28th | 6 Months | $275.00 |

| February | March 31st | 5 Months | $229.17 |

| March | April 30th | 4 Months | $183.33 |

| April | May 31st | 3 Months | $137.50 |

| May | June 30th | 2 Months | $91.67 |

| June | July 31st | 1 Month | $45.83 |

Note: The filing deadline always falls on the final business day of the month following the vehicle’s first introduction to public asphalt.

Step-by-Step Guide to Form 2290 E-Filing

By shifting from paper-based mail-in processes to an IRS-authorized e-file provider, you eliminate manual calculations and bypass long processing backlogs. Follow this step-by-step process to complete your filing:

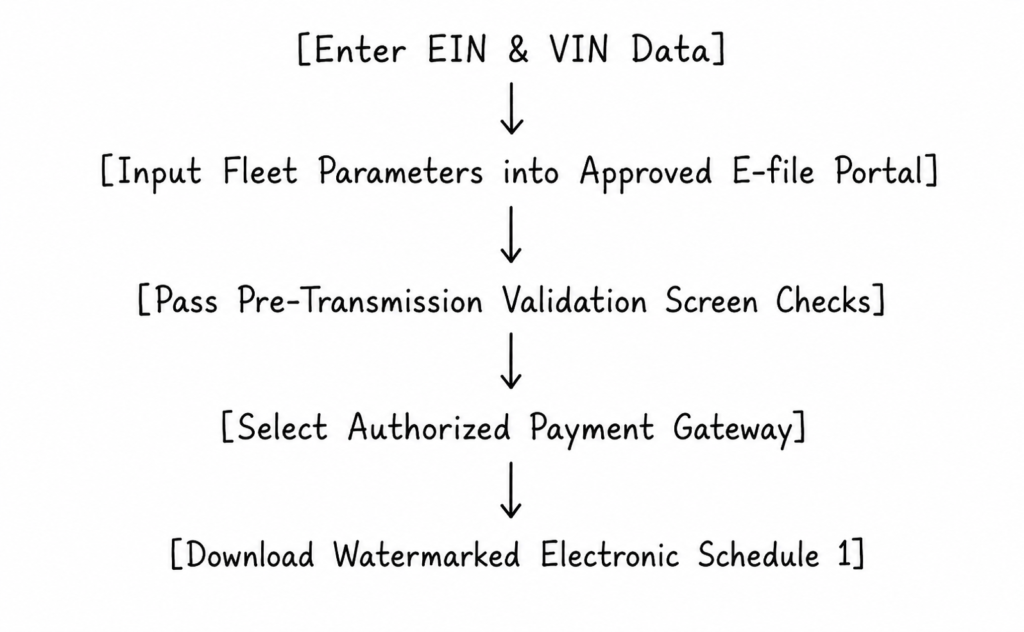

Step 1: Confirm Your Identity via EIN Data

The IRS will instantly reject any Form 2290 submitted with an independent operator’s personal SSN. You must secure a valid business Employer Identification Number (EIN) prior to setup. Ensure the legal name on your business documentation exactly matches your registration records to avoid automated database rejections.

Step 2: Input Vehicle Identification Data

Carefully type your vehicle’s 17-digit VIN into your e-file portal. Double-check this step; a simple typo will require a subsequent VIN correction filing to match your physical registration plates. Select your appropriate taxable gross weight bracket based on your maximum haul capacities.

Step 3: Identify Low-Mileage Suspended Assets

If you manage a backup yard tractor or a specialized regional vehicle that will travel fewer than 5,000 miles over the public highway network during the entire 12-month tax year (or under 7,500 miles for certified agricultural equipment), your vehicle qualifies as a Suspended Vehicle (Category W).

While you owe no tax on this vehicle ($0 balance), you are still legally required to list the truck and its VIN on your Form 2290 return.

Step 4: Authorize Your Payment Method

Choose a secure payment channel to send your tax funds to the U.S. Treasury:

- Electronic Funds Withdrawal (EFW): Direct debit from your business checking account via routing numbers.

- EFTPS: Payments processed independently through the U.S. Treasury’s secure Electronic Federal Tax Payment System portal.

- Credit/Debit Cards: Instant processing via certified third-party payment links.

Step 5: Download Your Watermarked Schedule 1

Once transmitted, the electronic system delivers your return to the IRS MeF interface. Within minutes of approval, an electronic stamped Schedule 1 featuring a official digital watermark is returned straight to your user account dashboard, ready to print for the DMV.

Safeguarding Your Records for the FMCSA Carrier Safety Audit

Completing your online filing is only the first step; maintaining clear records is crucial for ongoing regulatory compliance. Under Federal Motor Carrier Safety Administration (FMCSA) enforcement rules, every new operator must complete a comprehensive New Entrant Safety Audit within their first twelve months of active deployment.

During this safety audit, investigators cross-reference ELD log data and dispatch records against your historical tax receipts. If an auditor discovers an unfiled heavy vehicle or a mismatched VIN on your paperwork, it can trigger compliance penalties and affect your overall carrier safety rating. Keeping a digital file of your watermarked Schedule 1 documents protects your business from these compliance risks.

Frequently Asked Questions (FAQ)

Q1: Can I complete an online VIN correction filing if I notice a mistake on my approved Schedule 1?

A: Yes. If you spot a typo on your watermarked Schedule 1 receipt, you can file an official VIN Correction amendment directly through your IRS-authorized e-file provider. You will input the original, incorrect VIN, provide the accurate 17-digit character string, and resubmit the data. The IRS typically processes these correction updates within minutes, issuing a revised Schedule 1 so you can proceed with your state registration.

Q2: What happens if my truck exceeds the 5,000-mile exemption threshold late in the tax cycle?

A: If a truck originally filed as a suspended Category W asset passes the 5,000-mile mark on public highways, its tax exemption is voided. You must file an Amended Form 2290 Return by the final day of the month following the month your mileage crossed the threshold. You will pay the standard tax rate, prorated from the month the vehicle first entered service during that cycle.

Q3: If my business structure changes from a Sole Proprietorship to an LLC, can I still use my existing EIN to pay my Heavy Vehicle Use Tax online?

A: It depends on how the structural reorganization alters your federal tax classification. If you simply convert a sole proprietorship into a single-member LLC without changing your underlying tax structure, your existing EIN remains valid for heavy vehicle filings. However, if the transition involves setting up a multi-member corporation or partnership, the IRS usually requires you to apply for a new EIN, which must clear their database before you can file your next Form 2290.